District of Columbia

Minimum Auto Insurance Requirements in Washington, D.C.

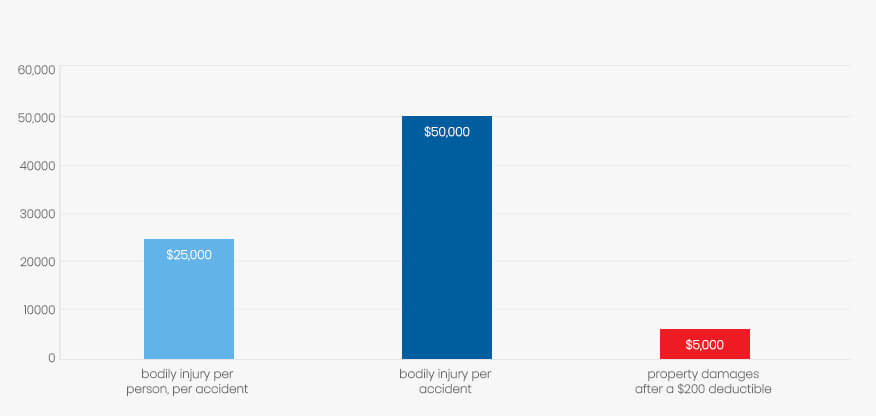

Drivers in Washington, D.C. must have at least the following amounts of uninsured motorist coverage.

| $25,000 for bodily injury per person, per accident |

| $50,000 for bodily injury per accident |

| $5,000 for property damages after a $200 deductible |

While these numbers are the minimum amounts of liability insurance a driver must have in the D.C. district, this doesn’t mean it’s the only amount they can carry. Insurance companies not only offer higher amounts but recommend it. It’s not unusual for a simple case of whiplash to result in a payout of $25,000 or more. Accidents that cause serious damage can result in much higher lawsuits.

Many auto accidents that involve serious injuries or fatalities can result in payouts in the six-figure range. There really is no such thing as being over-insured when it comes to auto liability insurance coverage. It’s always better to have too much coverage than not enough.

Top Three Counties (Wards) in Washington, D.C.

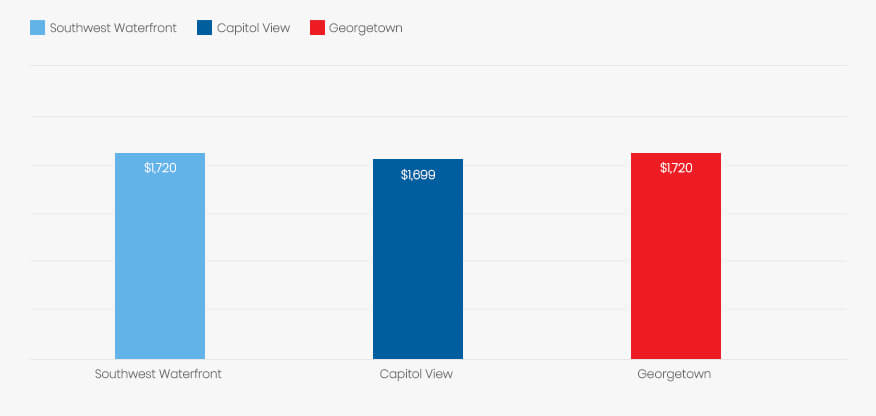

In most states, drivers can find fluctuations in the prices of car insurance from city to city. This is not the case in the Washington, D.C. area. The rates do not change much from one neighborhood to the next in the Capital Region. Here is an example of auto insurance rates in areas of the Washington, D.C. region. The rates are for a 45-year old, married woman with a good driving record.

Now that you know all the ins and outs of auto insurance in the Washington D.C. area, you can do some research and find an insurance company that offers the best policy for you and your family. Keep in mind that what’s best for your single neighbor may not be best for you and your family. Find an agent, discuss your options, and let the agent show you what the company has to offer. Although many insurance companies want you to call them or visit their office, some may give you quotes online.

Don’t make a decision based on one quote. Get quotes from several companies and compare both the coverage and the premiums to ensure you’re getting the best possible coverage for the best price. When it’s all said and done, you want to know that you’re walking away with good auto insurance coverage while still meeting your financial goals.