Known as the Lone Star State, Texas is the second largest state in the United States. It’s also a state that had almost 16 million drivers in 2015. With this many drivers traveling the Texas highways, it’s easy to understand the need for auto insurance laws. Continue reading and learn all about the Texas auto insurance requirements as well as ways you can lower your premiums more than you ever thought possible.

Summary of Auto Insurance in Texas

Texas is an at-fault insurance state that utilizes the tort system. What this means is that if you’re the responsible part in a car accident, you or your insurance company are responsible for paying for the damages. The other driver also has the right to sue you for damages. Texas drivers looking for auto insurance not only have various types of coverage from which to choose but also have many insurance companies. Here are the types of coverage offered in Texas.

Collision

This coverage pays for damages to your own vehicle if you hit or collide into another car.

Comprehensive

This coverage will pay for damages to your own vehicle due to accidents that were not a collision, such as hail damage, animal damage, falling objects, theft and vandalism.

Uninsured/underinsured drivers

This coverage offers you protection from accident-related damages caused by a driver without insurance or insufficient insurance.

Towing and labor

This pays for you to have your car towed if it’s involved in an accident or breaks down on and needs roadside assistance.

Liability coverage

This pays for the other person and their vehicle in an accident caused by you. It may include medical costs, car repairs or replacement, car rental and loss of wages. Liability insurance is usually offered as bodily injury and property damage.

While accident forgiveness, a program that prevents your premiums from increasing if you’re in an at-fault accident, is not available in all states, it is available through some Alabama insurance companies. Having accident forgiveness can actually save you a lot.

By “forgiving” the accident, your insurance premiums will not increase. Considering that accident claims stay on your insurance record for around five years, the savings can add up over this time period.

Requirements for Drivers in Texas?

Although there are various types of coverage available in Texas, the only ones that are required are below.

Bodily injury liability

Property damage liability

Although Texas law does not require you to purchase uninsured/underinsured motorist coverage, insurance companies recommend it be purchased as part of your auto insurance policy for a couple of reasons. Since Texas is a tort state, the person who causes the accident must pay for damages.

However, if the other driver doesn’t have insurance, your insurance may have to cover expenses, but your regular plan may not be enough. Secondly, approximately 20 percent of Texas drivers continue to drive without insurance despite the law.

When you purchase auto insurance, your insurance company will give you an insurance identification card. You must use the card as proof of insurance in the following situations.

Law enforcement requests it

If you’re involved in an accident

You register your car or new its registration

You get your driver’s license or renew it

Your car is inspected

If you don’t want to purchase auto insurance, other options are available to you

Purchase a surety body for at least two property owners in Texas

Deposit $55,000 in cash or securities with the Texas Comptroller

Deposit $55,000 in cash or cashier’s check with the county judge

Purchase a certificate of self-insurance

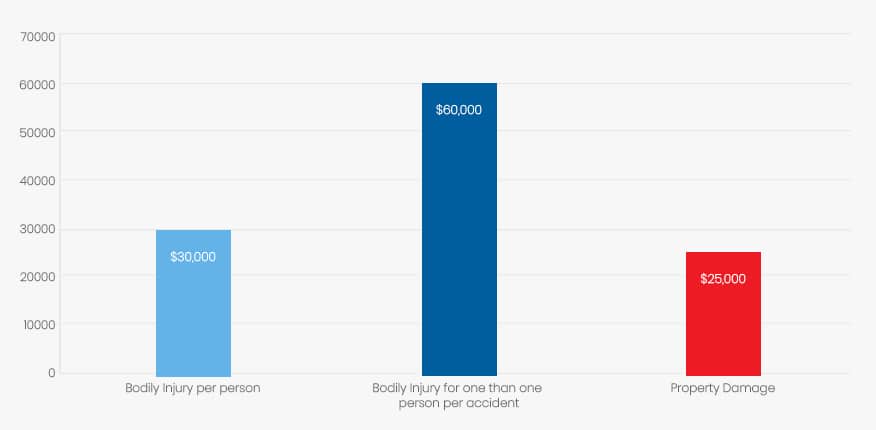

Minimum Auto Insurance Requirements in Texas

All drivers in Texas must carry the following insurance in at least the amounts listed,

Coverage

Minimum

Bodily Injury per person

$30,000

Bodily Injury for one than one person per accident

$60,000

Property Damage

$25,000

It’s important to understand that purchasing these amounts may be satisfying the state’s requirements, but it’s not offering you a great deal of coverage particularly when you consider the large number of car accident-related lawsuits. Additionally, if you are at the losing end of an expensive lawsuit, your insurance company can only protect you up to the limits of your coverage. Any remaining amounts due would need to be paid by you.

Are Any Auto Insurance Laws Specific to the state of Texas?

As a way to encourage residents to drive safely, the state requires Texas auto insurance companies give customers a five percent discount off their policies if they voluntarily complete a drug and alcohol awareness course approved by the Texas Education Agency.

Texas insurance companies may deny car insurance to drivers deemed to be high risk because of their claims history or driving records. These drivers may purchase insurance through the Texas Automobile Insurance Plan Association (TAIPA).

To be eligible for the TAIPA program, you must:

Live in Texas or have your car registered in Texas

Have a valid driver’s license or be in the process of getting one

State that at least two insurance companies refused you insurance in the previous two months

Drivers who purchase insurance through TAIPA will have coverage that meets the state’s minimum requirements, and will get this additional coverage.

$2,500 Personal Injury Protection

Uninsured/Underinsured motorist coverage for $30,000/$60,000/$25,000

To ensure that all drivers have insurance, the state utilizes a program called TexaSure. With this program, all law enforcement has to do is enter your identification number or license plate number, and the system will verify if you have valid insurance. For example, when your purchase your auto insurance in Houston, the insurance company sends verification to TexaSure, so they have this information in their system.

Ways to Lower Your Auto Insurance in Texas

We all want lower auto insurance premiums, but many don’t know what to do or how to get their premiums lowered. Being a safe driver is always the best way to get low premiums and keep them as low as possible. Being aware of the things that determine your insurance rates can help you to get lower premiums. Here are things that help determine your rates.

Your age

Marital status (younger drivers)

Driving record

Claims history

Where your vehicle is stored

How your vehicle is used

Your car’s year, make and model

Your credit scores

If your previously drove without insurance

Insurance companies also offer various types of discounts to help keep your premiums as low as possible. Bear in mind that each company may offer different discounts, or they may offer discounts that they fail to mention. Don’t be afraid to ask agents about potential discounts. They can be used as a great bargaining chip to encourage insurance agents to try to match their competitors.

When shopping for car insurance, shop around and speak with as many insurance companies as time permits. Compare coverage for coverage and discounts for discounts to see who will offer the lowest price for the best insurance. Here are some discounts offered by insurance companies in Texas.

Safety discounts for airbags and auto seatbelts

Discounts for antilock brakes or anti-theft devices

Defensive driver discount

Drive safe and save program

Good driving discount

Driver training discount

Good student discount

Multiple car discount

Auto renewal discount

Are Requirements Different for Part-Time or Full-Time Texas Residents?

The auto insurance requirements are aimed at full-time residents because part-time residents typically are full-time residents from another state. In Texas, you must have car insurance when you register your vehicle, and you must register your vehicle within 90 days of moving into the state. Prior to the 90 days, you will need to abide by the insurance laws from your state of residence.

Texas Rates Compared to National Average

Texas has several high-risk factors like flooding, tornadoes and traffic congestion, which contribute to higher premiums. Despite those factors, the Texas rates aren’t far off from the national average of $1,666. The average annual premiums for Texas auto insurance is about $1,700. Rates may be much lower in some areas and higher in others.

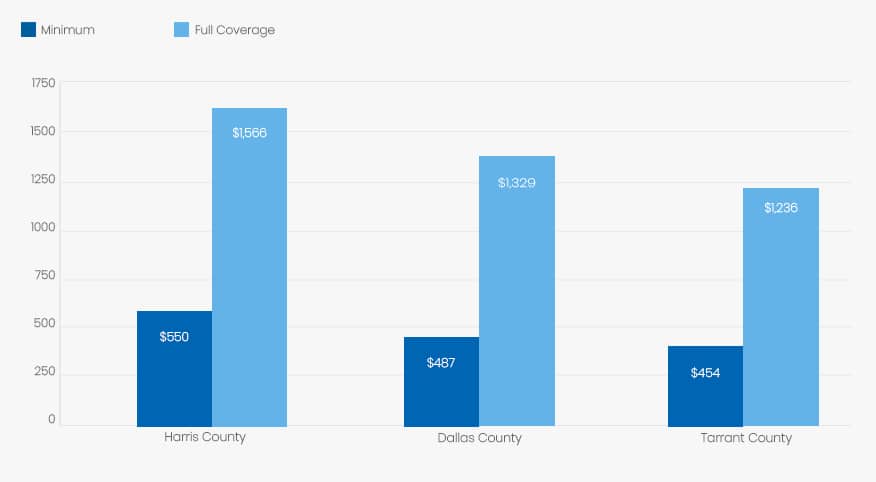

Average Rates in Top Three Texas Counties

Have you ever wondered if your insurance rates would be lower or higher if you lived in another city in Texas or even another county? They probably would be different, but it’s hard to determine what the difference would be. To demonstrate, I used a 45-year old married female as my example. This female is a good driver.

I have listed the rates from three of Texas’s largest counties. The rates are for full coverage and just the liability amounts required by the state. As you can see, there is a slight difference. Keep in mind that other cities throughout the state may vary even more.

County

Minimum Coverage

Full Coverage

Harris County

$550 for state minimum requirement

$1,566 for full coverage

Dallas County

$487 for state minimum requirement

$1,329 for full coverage

Tarrant County

$454 for state minimum requirement

$1,236 for full coverage

Conclusion

With all the information, you now have about Texas car insurance and how it works, you should be all set to start shopping around for insurance policies. For the best rates possible, ask each company what they offer in the way of discounts and savings promotions. What you may save in premiums can pay for more protection or just give you more money in your pocket. It’s a win-win situation!