ON THIS PAGE

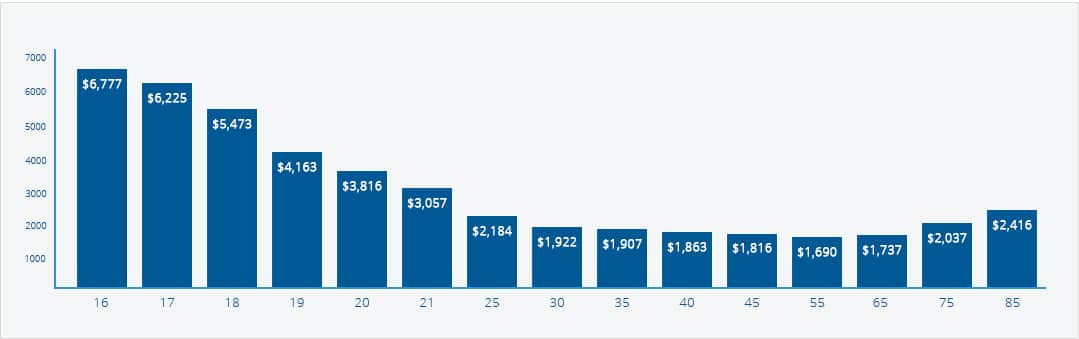

Average Auto Insurance Premium Per Year For Different Ages

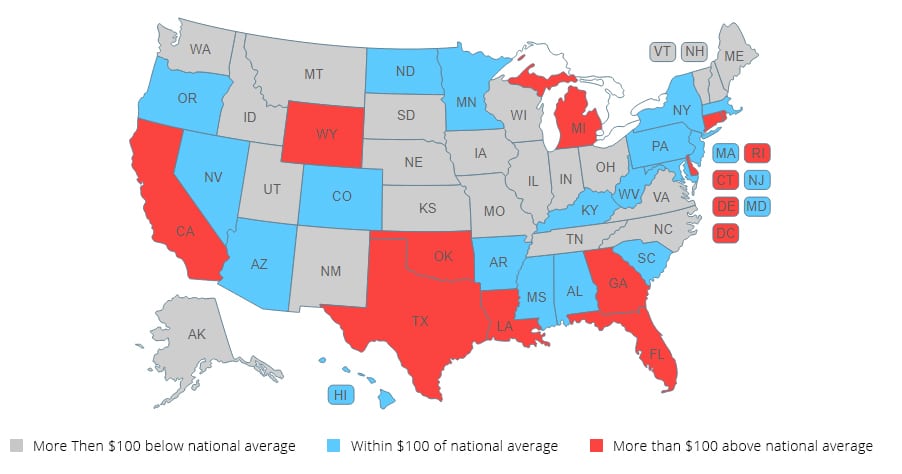

Your Insurance Rates by State

As stated above, where you live and your lifestyle will affect your insurance rates. Here are examples of the three most and least expensive states for car insurance for a 35 year old married man:

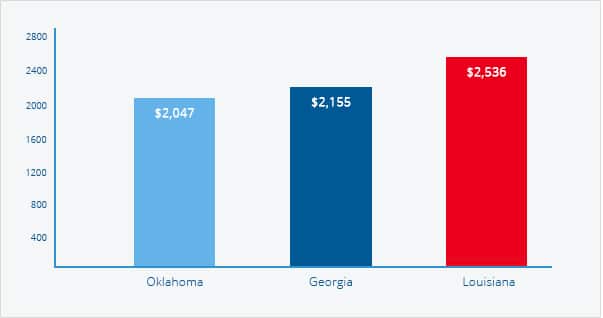

The top three states with the highest car insurance rates:

| States | Highest Car Insurance Rates |

|---|---|

| Louisiana | $2,536 |

| Oklahoma | $2,047 |

| Georgia | $2,155 |

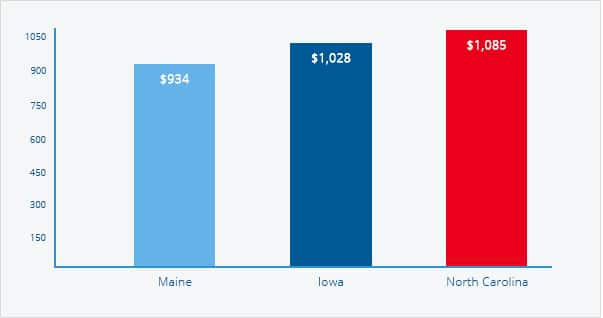

The top three states with the highest car insurance rates:

| States | lowest Car Insurance Rates |

|---|---|

| North Carolina | $1,085 |

| Iowa | $1,028 |

| Maine | $934 |

Now, when you factor in the type of vehicle driven it can boost your premium considerably. Although Oregon ranks right about in the middle for average car insurance if you’re a 35 year old man driving a Mercedes-Benz CL65 AMG coupe you can expect an insurance rate over $5,800! Likewise, if you drive a clunker and aren’t worried about replacement costs it can lower your overall insurance costs considerably.

Within a state the zip code can also make a difference in how cheap your car insurance rate is. A survey reported by CBS shows the following highest and lowest zip codes for car insurance rates:

Most expensive zip codes:

Cheapest zip codes:

Cheapest Car Insurance Companies

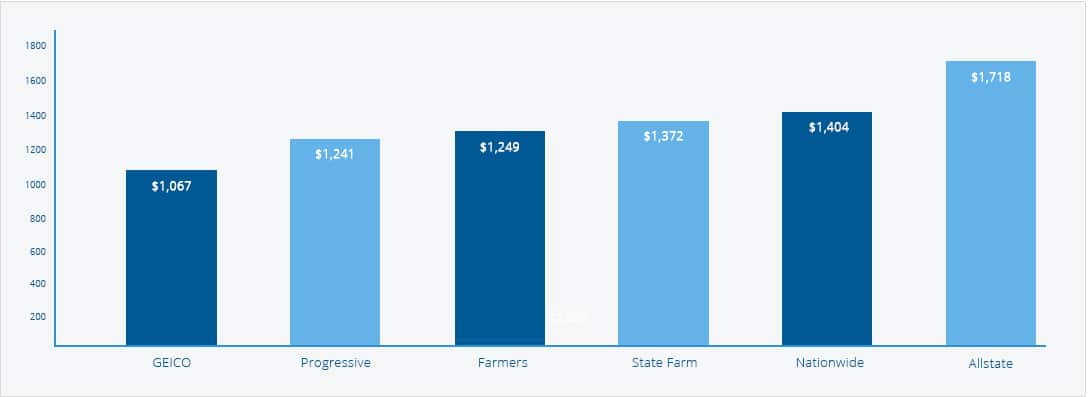

Again, the cheapest companies depend on where you live. Using our example of the 35 year old married man driving a 2015 Honda Accord, the following major companies were the cheapest rates. Keep in mind this is a national average, so a lot depends on your state of residence as well as the zip code in which you live:

| Companies | Insurance Rates |

|---|---|

| Geico | $1,067 |

| Progressive | $1241 |

| Farmers | $1249 |

| State Farm | $1372 |

| Nationwide | $1404 |

| Allstate | $1718 |

Lesser known companies aren’t necessarily higher though. For example, Erie Insurance, which is based in only nine states, was only $1052 per year. Likewise, American Family is only available in Washington and Colorado and their annual rate is only $1099. That’s why it pays to get an online quote from a site that compares many companies at the same time!