ON THIS PAGE

Auto Insurance in Denver

Unmarried Male, 21, No Violations in 3 Years – Lowest/Highest Coverage

This chart contains the results of our Denver insurance quotes analysis. We searched dozens of insurance companies that operate throughout the state of Colorado for insurance rates. After getting quotes from numerous providers in Colorado, we narrowed our results down to the eight trusted companies with the best insurance rates available. As usual, insurance rates in Colorado differ from city to city and depend on a number of factors.

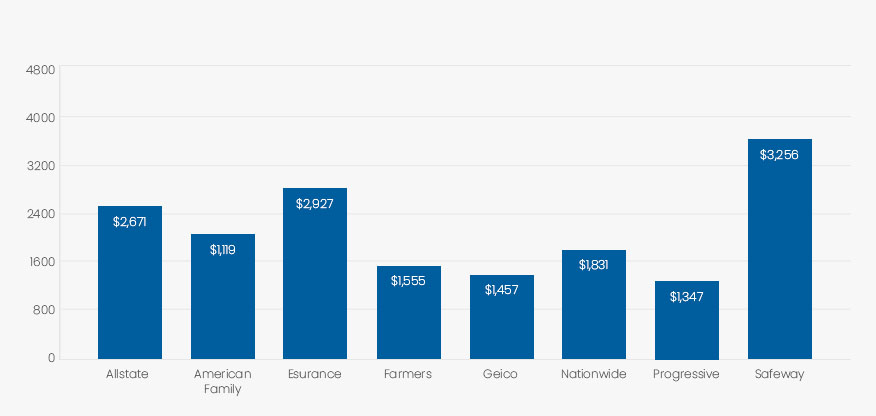

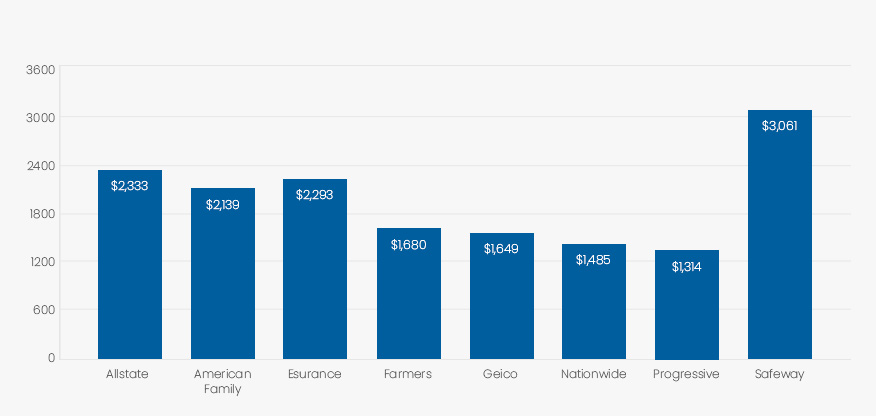

The first scenario is for a single male in his late 20’s who hasn’t had any violations within the past three years, drives at least ten miles each day to work, and is seeking the lowest coverage possible. Living in Denver, he can get the lowest coverage insurance plan with Progressive for just $922, which is the lowest rate. The highest rate of $3,694 is from Safeway. If the same male was looking for the most coverage available, Progressive provides the least expensive at $1,400 and Esurance costs the most at $2,944.

| Unmarried Young Male | Lowest Coverage |

| Allstate | $2,488 |

| American Family | $2,119 |

| Esurance | $2,927 |

| Farmers | $1,555 |

| Geico | $1,457 |

| Nationwide | $1,831 |

| Progressive | $1,347 |

| Safeway | $3,694 |

| Unmarried Young Male | Highest Coverage |

| Allstate | $2,539 |

| American Family | $2,295 |

| Esurance | $2,944 |

| Farmers | $1,747 |

| Geico | $1,597 |

| Nationwide | $1,745 |

| Progressive | $1,400 |

| Safeway | N/A |

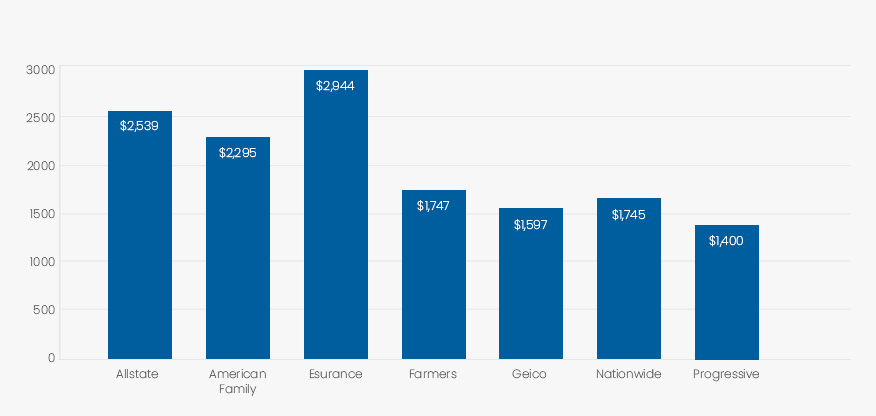

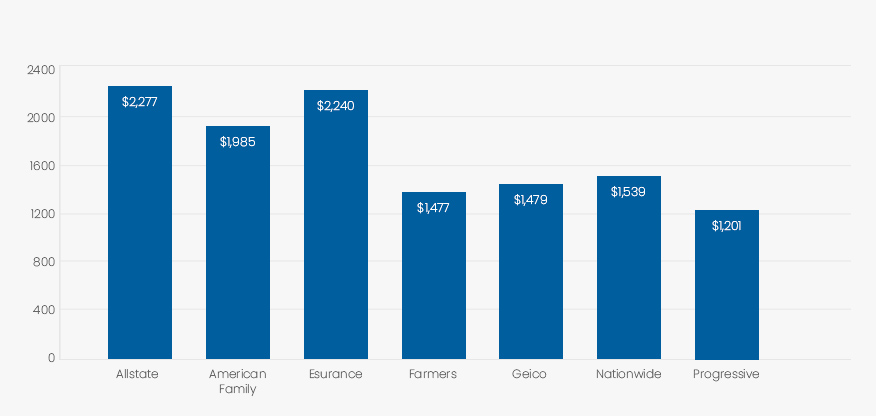

Unmarried Female, 21, No Violations in 3 Years – Lowest/Highest Coverage

Now let’s take a look at the rates for a single female looking for the least amount of coverage allowed by state law, as well as the highest amount of coverage. The woman in this scenario is approximately 30 years old and hasn’t had any accidents where she was at fault in the previous three years. In addition, she drives 10 miles to work. In Denver, Progressive offers the lowest rate available for both minimum and full coverage, with the minimum costing $1,201 and the full coverage plan costing $1,314. American Family has the highest rate of $2,277 for minimal coverage and $3,061 for the highest coverage plan.

You may have noticed that insurance for males is more expensive than for females with the same scenario. This is because men of a certain age are considered more reckless than women in the same age group, who are more cautious while driving. However, as they age, men’s insurance costs begin to normalize. The rates for older women will be higher than a man’s in the same age group, but not by much.

| Unmarried Young Female | Lowest Coverage |

| Allstate | $2,277 |

| American Family | $1,985 |

| Esurance | $2,240 |

| Farmers | $1,477 |

| Geico | $1,479 |

| Nationwide | $1,539 |

| Progressive | $1,201 |

| Safeway | N/A |

| Unmarried Young Female | Highest Coverage |

| Allstate | $2,333 |

| American Family | $2,139 |

| Esurance | $2,293 |

| Farmers | $1,680 |

| Geico | $1,649 |

| Nationwide | $1,485 |

| Progressive | $1,314 |

| Safeway | $3,061 |

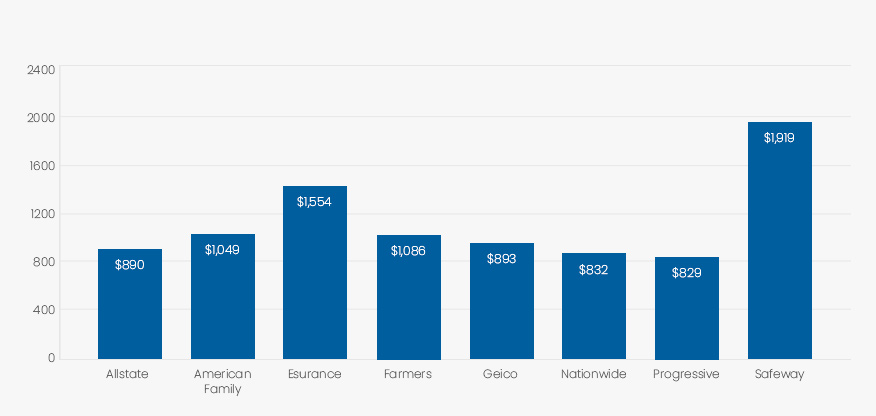

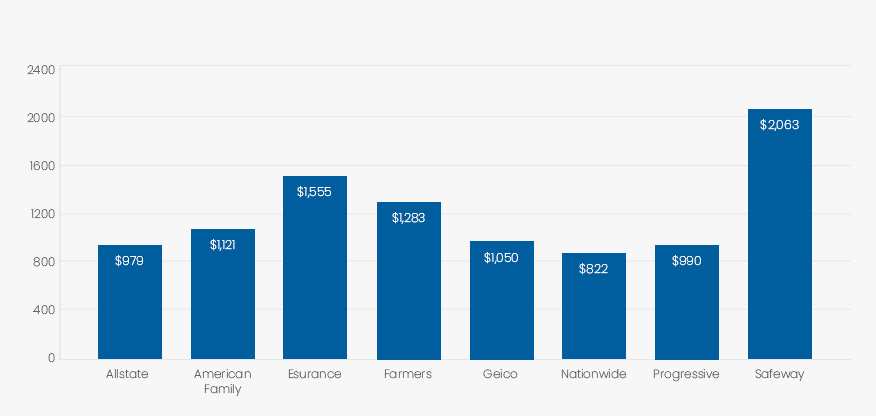

Married Male, 35, No Violations in 3 Years – Lowest/Highest Coverage

The chart we put together clearly shows that, for a 35-year-old married male with no violations in three years, the lowest rate for the least amount of coverage is $829 from Progressive and the highest is $1,919 from Safeway. Nationwide has the lowest rate of $822 for the highest coverage amount and Safeway in Denver has the highest rate for the highest coverage; $2,063.

You may be wondering why someone who is single has to pay more insurance than someone who fits the same profile but is married. The truth is, average singles pay 10% more in premiums than those who are married because single drivers are considered a higher risk, as they are more likely to file claims.

| Married Male | Lowest Coverage |

| Allstate | $890 |

| American Family | $1,049 |

| Esurance | $1,554 |

| Farmers | $1,086 |

| Geico | $893 |

| Nationwide | $832 |

| Progressive | $829 |

| Safeway | $1,919 |

| Married Male | Highest Coverage |

| Allstate | $979 |

| American Family | $1,121 |

| Esurance | $1,555 |

| Farmers | $1,283 |

| Geico | $1,050 |

| Nationwide | $822 |

| Progressive | $990 |

| Safeway | $2,063 |

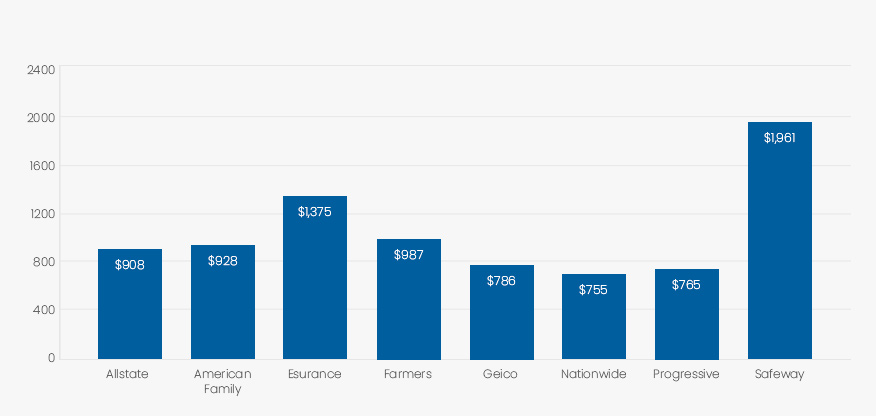

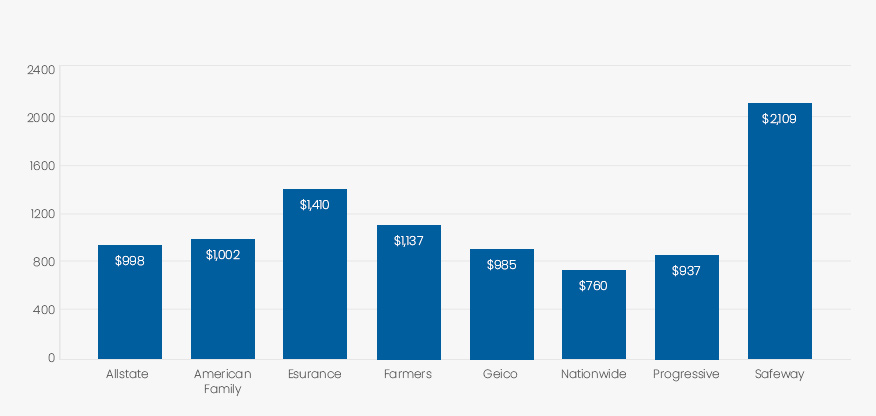

Married Female, 21, No Violations in 3 Years – Lowest/Highest Coverage

A married female living in Denver, without any violations, and who doesn’t drive for work can get minimum insurance coverage from Nationwide for as little as $755 and full coverage from Nationwide for just $760. The most expensive of these plans comes from Safeway, with minimum coverage for $1,961 and full coverage for $2,109.

| Married Female | Lowest Coverage |

| Allstate | $908 |

| American Family | $928 |

| Esurance | $1,375 |

| Farmers | $987 |

| Geico | $786 |

| Nationwide | $755 |

| Progressive | $765 |

| Safeway | $1,961 |

| Married Female | Highest Coverage |

| Allstate | $998 |

| American Family | $1,002 |

| Esurance | $1,410 |

| Farmers | $1,137 |

| Geico | $985 |

| Nationwide | $760 |

| Progressive | $937 |

| Safeway | $2,109 |